March 2021 - Monthly Market Update

/Monthly Update || March 2021

“Nothing goes in one direction forever … Cycles always prevail eventually … Just about everything is cyclical.”

Opening Remarks

Greetings from inside Ikigai Asset Management¹ headquarters in Marina del Rey, CA. We welcome the opportunity to bring to you our thirtieth Monthly Update and hope these are helpful in better understanding some of what we’re doing and what we’re seeing. We have the privilege of deploying capital on behalf of our investors into a new technology and asset class that we believe will fundamentally change the world and create trillions of dollars of value in the process.

We believe we are obligated to be shepherds of this technology – to help the world better understand the powerful potential of DLT and crypto assets, and to fund and be an ambassador for DLT projects that will change our lives forever.

To that end, February continued the streak of 5+ months of stunningly positive news flow, including arguably the single most positive event in Bitcoin history – Elon Musk buying $1.5bn of Bitcoin on TSLA’s balance sheet. But that’s not to sleep on many of the other news events that occurred this past month because there were many significant positive occurrences. The multiyear Tether saga with the NYAG has come to a conclusion that was unequivocally bullish for crypto broadly. An $18.5mm fine could barely be considered a slap on the wrist, all things considering. Importantly, Tether did not admit to any wrongdoing and committed to quarterly audits of reserves going forward. While the near-term price reaction to this news was weak, I believe this is massively bullish for Bitcoin and crypto broadly over the coming months and years. Tether was one of the single largest risk factors preventing more institutional capital from flowing into the space. I believe the removal of this risk will be the backdrop for Bitcoin to test $100k and beyond.

While Bitcoin and crypto broadly experienced step changes in adoption and investability in February, the macro backdrop continued its own dynamic evolution.

Source: TradingView. As of 2/28/21.

I know what you’re probably thinking looking at that – “what’s everyone freaking out about?” And generally I agree. That looks like about a 40-year downtrend that fell out of the bottom of the channel last year and has now popped back up in the middle part of the downward channel. Granted, that is nearly a double off the bottom in April of last year. And there are a few things many macro investors are taking notice of with some degree of concern, namely:

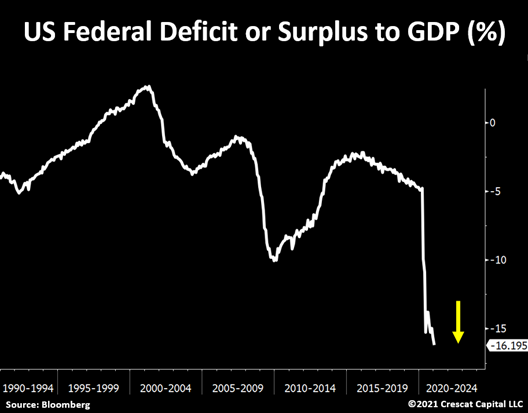

1) US deficit to GDP looks really scary.

As of 2/27/21.

2) It’s going to get worse.

3) So the US Treasury will need to issue a LOT of debt.

As of 12/29/20.

4) And that’s a problem because foreigners aren’t buying many Treasuries these days.

As of 2/20/21.

5) Which has led many to the conclusion that the Fed’s current pace of QE at $120bn/month is not enough, and more will be needed. If more will be needed, that leaves the market hungry for more commentary from Fed officials and laser focused on the functioning of the Treasury market, or said differently, on edge.

6) So when this sort of thing happens:

7) People freak out.

Source: TradingView. As of 2/28/21.

Do I think this freak out has much legs to it? No, I don’t, although I’m certainly willing to change my mind. I think the market is throwing a mini tantrum to force the Fed into further clarifying their intentions regarding the pace of asset purchases and the future change (or lack thereof) in interest rates. I believe the Fed can put interest rates more or less wherever they want, until something breaks and they can’t do that anymore. But I don’t think that time is this year, and likely not in the first part of this decade. So for now, the Fed will likely increase its jawboning and likely make some changes to some of the more nuanced aspects of QE so as to better accomplish their goals while minimizing market disruption. If the market signals that they’re still not doing “enough”, then they’ll do more of whatever is needed until the market is placated. That is where we find ourselves – with global financial markets entirely beholden to monetary and fiscal policies and thus dictating those policies, because the rule makers are in turn beholden to financial markets.

Bitcoin is intimately involved in this. Bitcoin loves QE. It requires it. Bitcoin hates QT. It’s terrified of it. For Bitcoin to go from $1tn to $2tn and beyond, it’s likely going to require increasingly more egregiously irresponsible monetary and fiscal policy. This acts as a forcing function for capital to flow into hard assets, and Bitcoin is the hardest money in human history. To the extent the Fed and Treasury get backed further and further into a corner of having to do more and more, an investor’s conviction level in Bitcoin should grow alongside their conviction that the Fed and Treasury have no choice. Bitcoin is purpose-built for a time such as this.

These tantrums we have along the way, mini or otherwise, are worth paying attention to, especially for those of us who manage other people’s money in this asset class for a living. Because they can cause price volatility. But read the highlights below and take a step back. We’re really just getting started.

Invest

Ikigai is currently fielding interest from new investors globally. We are open to international and qualified accredited U.S. investors (including self-directed IRAs).

Contact us to see if you qualify.

February Highlights

TSLA Buys $1.5bn of Bitcoin on Balance Sheet

Microstrategy Raises $1.05bn Convert to Buy Bitcoin; Purchases 19,452 Bitcoin at $52,765

Square Buys $170mm of Bitcoin on Balance Sheet

Tether Settles Longstanding Case with NYAG for $18.5mm; Does Not Admit Wrongdoing; Agrees to Future Quarterly Audits of Reserves

BNY Melon to Custody Crypto

MasterCard to Enable Crypto Purchases for All Merchants

Canadian Bitcoin ETF BTCC Begins Trading, Sees Strong Inflows

Bitcoiner Cynthia Lummis Named to Senate Banking Committee

Former TD Ameritrade Head of Digital Assets Named Fed’s Chief Innovation Officer

BlackRock Begins Buying Bitcoin

Microstrategy Buys $10mm Bitcoin at $33,810

Coinbase Files S-1

Bitcoin Company Casa Raises $4mm Seed Round Led by Fidelity’s Avon Ventures

Deutsche Bank to Offer Crypto Custody and Prime Brokerage

BlockFi Raises Series D at $2.85bn Valuation

Dapper Labs Raises $250mm at $2bn Valuation

Jack Dorsey and Jay-Z Allocate $23.5mm in Bitcoin to Fund Development

Miami Mayor Activates Bitcoin Across the City, Including Treasury, Employees, Taxes & Fees

BitPay Card Adds Support for Apple Pay

Bitfinex Repays $550mm Outstanding Loan from Tether

Ruffer Sells $750mm of Bitcoin After Original $740mm Position Doubles in Two Months

| Asset Class | Feb | Jan | YTD | Q4-20 | Q3-20 | Q2-20 | 2020 | Instrument |

|---|---|---|---|---|---|---|---|---|

| Bitcoin | 36% | 14% | 56% | 169% | 18% | 42% | 303% | BTC |

| NASDAQ | 0% | 0% | 0% | 13% | 12% | 30% | 48% | QQQ |

| S&P 500 | 3% | -1% | 1% | 12% | 8% | 20% | 16% | SPX |

| Total World Equities | 3% | 0% | 2% | 15% | 8% | 19% | 14% | VT |

| Emerging Market Equity | 1% | 3% | 4% | 17% | 10% | 17% | 15% | EEM |

| Gold | -6% | -3% | -9% | 1% | 6% | 13% | 25% | GLD |

| High Yield | -1% | 0% | -1% | 4% | 3% | 6% | -1% | HYG |

| Emerging Market Debt | -3% | -2% | -5% | 5% | 2% | 13% | 1% | EMB |

| Bank Debt | 0% | 0% | 0% | 2% | 2% | 4% | -2% | BKLN |

| Industrial Materials | 11% | -2% | 8% | 14% | 11% | 10% | 16% | DBB |

| USD | 0% | 1% | 1% | -4% | -4% | -2% | -7% | DXY |

| Volatility Index | -15% | 45% | 23% | -14% | -13% | -43% | 66% | VIX |

| Oil | 17% | 7% | 25% | 17% | 1% | -17% | -68% | USO |

Source: TradingView. As of 2/28/21.

When The FUD Well Starts To Run Dry, Go to ESG

In last month’s Monthly Update letter, I unpacked a number of different potential risks to Bitcoin and presented a framework on how to approach those risks. If you haven’t read it, I suggest you do. I believe it was one of the better letters I’ve written. I also went on NLW’s podcast to discuss those topics and more. I think it was one of the better pods I’ve done. One risk, or perhaps “negative aspect”, I didn’t address which has reared its head again over the last several weeks is “Bitcoin is bad for the environment”. This is not the first, second or third time we’ve seen this movie. But from time to time throughout the years, the amount of electricity used by the Bitcoin network is brought up as a reason why Bitcoin cannot succeed. Allow me to unpack some of my views on the topic, and to present this as a definitive guide to understanding Bitcoin’s energy usage.

First, I want to present a few of the news articles that got traction in recent weeks. If you haven’t read them, it’s worth a quick flip.

The Guardian: “Electricity Needed to Mind Bitcoin Is More Than Used By Entire Countries”

Bloomberg: “Bitcoin’s Long-Term Value Doubted Due to ESG, Tighter Regulation”

To quote Mark Twain, “there is no such thing as a new idea. It is impossible. We simply take a lot of old ideas and put them into a sort of mental kaleidoscope. We give them a turn and they make new and curious combinations.” So to that end, I want to include a few prior written rebuttals to the “Bitcoin uses too much energy” argument. If you haven’t already, I suggest you read them. They’re excellent.

Now that we have that out of the way, my points are as follows:

Bitcoin economically incentivizes finding the cheapest electricity on earth. While it is impossible to know exactly what the blended Kw/h cost of electricity is for Bitcoin mining, the much quoted Cambridge University analysis assumes $0.05 Kw/h. Below is a map of 2019 electricity prices by state. Note that there is no state in the United States that has $0.05 power on average. Thus, on average, every state is too expensive to profitably compete in Bitcoin mining.

Source: Global Energy Institute. February 2020.

That’s not to say there isn’t any Bitcoin mining going on in the U.S. There. Is. Plenty. But these operators, like all Bitcoin miners, must find the cheapest power possible in order to be profitable. That means finding electricity that would otherwise go unused. Electricity sourced far away from demand centers. Bitcoin miners could never profitably compete with people that need electricity to cool their home or heat or their stove. They must find the cheapest power out there. Comparisons like “Bitcoin uses as much electricity as Argentina” are just disingenuous. They imply that Bitcoin is stealing electricity from people that need it. That is simply not true. Bitcoin finds the energy that no one is using.

Bitcoin acts like a battery. This point often gets misunderstood by casual observers. Bitcoin mining allows electricity (which oftentimes would have otherwise been wasted) to be converted into a fungible asset that last forever and can be sent anywhere in the world instantaneously and then converted back into energy (i.e., sell Bitcoin for cash then use the cash to buy electricity). Gold is good at transferring value across time but not space. Fiat is good for transferring value across space but not time. Bitcoin is good at transferring value across space and time, and Bitcoin mining is how electricity is converted into that unit of value. This characteristic of Bitcoin should not be taken lightly. The world has never had anything like it before.

Some assumptions and comparisons made by “Bitcoin is bad for the environment” folks are questionable at best. Several articles eschewing Bitcoin mining include statements that most of Bitcoin mining is powered by coal. There is no evidence of this. While there is no way to know exactly how much mining is powered by various energy sources, there are estimates. Cambridge says 39% comes from renewable energy with 76% of miners using at least some renewable energy. Coinshares says more than 74% of mining is powered by renewables. 39% and 74% is a pretty wide margin. If 74% is correct, is it really that big of a deal, especially if the expectation is for that number to go higher over time? If all Bitcoin mining was powered entirely by renewable energy, would the ESG crowd have anything to complain about?

Other articles include comparisons like “a single Bitcoin transaction has the same carbon footprint as 680,000 Visa transactions.” Again, this is disingenuous. They’re two totally different things. Visa is a thin slice of unsettled IOUs that sits on top of ACH, Fedwire, SWIFT and banks. Bitcoin is a standalone settlement layer that operates in a totally trustless manner. Two totally different things.

The last point I’ll make is several articles misrepresent what the future of Bitcoin mining will be, likely because the author doesn’t understand what they’re talking about in conjunction with trying to generate clicks (as journalists do). Bitcoin mining is a structurally shrinking business unless you are highly bullish on fees and bearish on Layer 2’s like Lightning and Liquid. As the block reward continues to be cut in half every four years, miners will make less and less money from mining and more and more from fees. Fees on the Bitcoin blockchain will increase, causing more transactions to begin settling on L2’s or other networks entirely. Eventually, miners are no longer generating sufficient profits and will lay down mining rigs, which in turn decreases mining difficulty, increases profitability, and an equilibrium is found. So linearly extrapolating the current energy usage for Bitcoin into the future is highly likely to be incorrect.

All electronic technology requires… electricity. This may seem self-evident, but the ESG crowd seems to be ignoring it.

As of February 2021.

I understand why many people are focused on climate change and in turn, carbon footprints. We as a species should be acutely working towards making sure our planet is in good shape forever. We should be diligently moving towards more clean, renewable fuel sources and away from hydrocarbons. That’s true across the board, regardless of what the energy is being utilized for. We should especially be looking for low hanging fruit – places to reduce the carbon footprint without meaningfully altering how we live our lives. But if we really wanted to reduce the carbon footprint, why not shut down the internet in its entirety? Why not outlaw all hydrocarbon-fueled vehicles? Because that’s impractical. Even the most zealous environmental proponent isn’t demanding we shut down the internet to save the planet, right? So, once we have some of the facts properly presented and contextualized, the underpinning of “Bitcoin mining is bad for the environment” is actually a question of *whether Bitcoin is important*. Which leads me to my final point.

Whether Bitcoin is a worthy expenditure of energy is a matter of opinion. Bitcoin is a non-sovereign, hardcapped supply, global, immutable, decentralized, digital store of value. It is an insurance policy against monetary and fiscal policy irresponsibility from central banks and governments globally. The world has never had anything like Bitcoin before. It is truly incomparable. The Bitcoin blockchain operates in a trustless manner utilizing a cryptographic consensus mechanism called Proof of Work, which predates Bitcoin itself. The “work” portion of PoW is the provision of electricity to secure transactions on the Bitcoin blockchain. While there are other consensus mechanisms which require less electricity than PoW, none of them have been proven to work at scale in a sufficiently decentralized manner like Bitcoin has. There are some people out in the world, and potentially some of the authors of the “Bitcoin is bad for the environment” pieces, that believe *any* expenditure of energy on Bitcoin is a waste. A single charcoal briquette with an ASIC miner plugged into it is one briquette too many. A single turn of a windmill that goes to Bitcoin mining is one turn too many, because that turn could be used to power data centers working on curing cancer with machine learning. And then there are people that think Bitcoin is one of the most important inventions in human history, one of the single most noble projects on Earth and worth every joule of energy expenditure required and then some. Most folks end up somewhere between those goalposts and where you end up is heavily correlated with how much research you’ve done. So keep doing your homework and arrive at your own conclusion.

Market Update – Liquid Crypto Asset Investing

| Symbol | February | January | YTD | Q4-20 | Q3-20 | Q2-20 | Q1-20 | 2020 | 2019 | % ATH |

|---|---|---|---|---|---|---|---|---|---|---|

| BTC | 36% | 14% | 56% | 169% | 18% | 42% | -11% | 303% | 92% | N/A |

| ETH | 8% | 78% | 92% | 105% | 59% | 69% | 3% | 469% | -3% | N/A |

| XRP | -16% | 124% | 89% | -9% | 38% | 1% | -10% | 14% | -45% | -89% |

| BCH* | 11% | 10% | 22% | 31% | 5% | -1% | 26% | 71% | 30% | -85% |

| EOS | 19% | 12% | 33% | 1% | 9% | 6% | -14% | 1% | 0% | -85% |

| BNB | 373% | 18% | 461% | 27% | 90% | 22% | -8% | 172% | 123% | N/A |

| XTZ | 20% | 41% | 70% | -9% | -7% | 46% | 20% | 49% | 192% | -13 |

| XLM | 33% | 138% | 217% | 71% | 12% | 64% | -10% | 184% | -60% | -56% |

| LTC | 27% | 4% | 32% | 169% | 12% | 6% | -5% | 202% | 36% | -56% |

| TRX | 44% | 18% | 70% | 2% | 61% | 41% | -13% | 101% | -29% | -84% |

| Aggregate Mkt Cap | 39% | 29% | 80% | 122% | 32% | 44% | -5% | 301% | 51% | N/A |

| Aggr Alts Mkt Cap | 45% | 65% | 139% | 56% | 58% | 45% | 4% | 274% | -1% | -3% |

Source: CoinMarketCap. As of 2/28/21. BCH includes SV.

Bitcoin specifically and crypto broadly are off to another hot start in 2021, up 56% and 139% YTD, respectively. As discussed, that price action has come on the back of red-hot news flow that continues to arrive at an unimaginable pace. But it’s not entirely crypto specific news driving BTC and crypto price action. After several months of deprecating “It’s All One Trade™”, an updated version is worth presenting. Below is SPX (red), EEM (purple), CNH (inverted pink), DXY (inverted green), oil (turquoise), 2s10s (blue) and BTC (orange) since late September.

Source: TradingView. As of 3/1/21.

Note a pretty tight channel until the dollar started strengthening in late January. Then a bit more decoupling in the last couple weeks of February as equities and the renminbi rolled while BTC, oil and 2s10s (inflation expectations) pushed higher. Just over the last few days we’ve had all of it appearing to come back together (excluding the dollar). It’s all worth paying close attention to, as Bitcoin is intimately involved in the underlying theme driving these correlations – reflation driven by a reopening of the economy on the back of vaccine distribution in conjunction with historically loose monetary and fiscal policies. That theme will likely serve as the primary backdrop for financial markets through the remainder of this year.

Source: TradingView. As of 3/1/21.

Bitcoin price action in February was defined by “The Elon Candle”, which at $7,293 of daily gain on February 8th makes it the largest daily $ gain in Bitcoin history. Of lesser importance but still noteworthy was the violent pullback on February 22nd followed by a leak lower into month-end. Particularly interesting about this month-end slide was that it occurred after the announcement of Tether’s settlement with the NYAG. From what I could tell, traditional markets were freaking out about a bad Treasury auction and that overshadowed the Tether event. But I want to be clear – the Tether settlement was VERY bullish for crypto. In my opinion, having the opportunity to buy Bitcoin lower than the price was before the Tether announcement will likely be viewed as an attractive entry with just a bit of hindsight.

The viciousness of the pullback in February should not be glossed over. It was the largest liquidation event in crypto history by dollar amount.

Source: Bybt.com. As of 3/1/21.

Over $7.2bn of longs were liquidated over three days across all names. That’s a massive event. The liquidations plus the price decrease served to reduce Open Interest on Bitcoin from $19bn to $15bn.

Source: Bybt.com. As of 3/1/21.

The market at least gave you some clues that it was overheated before the correction. Below is the funding rate of various Bitcoin Perpetual Swaps. It’s a little noisy but the overall takeaway is clear – that big bubble in mid-Feb was traders getting greedy. Worth noting this looks much better currently.

Source: coinalyze.com. As of 3/1/21.

Another notable market occurrence this month was the GBTC NAV premium, which collapsed from 12% at Bitcoin’s ATH in price down to zero, and even briefly traded negative. The “GBTC NAV trade” discussed at length in previous Monthly Updates, is now in the difficult part of the trade, where the unlocked GBTC share supply that was created at par using borrowed BTC must now find demand in the secondary market. Sufficient demand to soak up all this supply may prove difficult to come by in the coming months, as cheaper competitors to GBTC have popped up and are gaining traction, including a full-blown Canadian Bitcoin ETF. In my view, those that are long GBTC after borrowing BTC to create shares have their work cut out for them in the coming quarters. I would not expect GBTC to trade at a significant premium for any material amount of time the rest of this year.

Source: Glassnode. As of 3/1/21.

Speaking of that Canadian ETF, their Bitcoin holdings are growing rapidly.

Source: Glassnode. As of 3/1/21.

Where does that put Bitcoin in the bigger picture? Well Bitcoin just closed its 5th consecutive month positive, only the fourth time that’s ever happened. Six consecutive positive months hasn’t happened since April 2013. And you’re coming up on the worst month of the year for Bitcoin seasonality.

Source: @JohnStCapital. As of 2/28/21.

Is Bitcoin overheated here? Meh, maybe. A lot less overheated after a 26% pullback and billions of liquidations though. If we weren’t in the midst of a raging bull market and if you weren’t coming off the back of arguably the single most bullish month in crypto history, you might be a little more worried about something like an elevated weekly RSI. But check out the comparison to 2017. Bitcoin appears to be right on schedule.

Source: TradingView. As of 3/1/21.

ETH and many Alts have jumped out to an even hotter start than BTC, as the apparent massive inflows into BTC have served to bolster investors’ confidence in stepping further out on the risk spectrum in crypto. The driver of ETH’s YTD outperformance has been clear – DeFi. The aggregate DeFi market cap shown below has increased an eyewatering 235% YTD.

Source: Coingecko. As of 3/1/21.

This might feel overdue for a correction, except we just had a 25% pullback. And then you look at DeFi dominance (DeFi market cap as a percent of total market cap) and see that it’s only 4.7%, up from ~1% a year ago. And then you put that 4.7% number into context that, outside of Bitcoin as a monetary inflation hedge, DeFi is THE only narrative in crypto with legit traction and real usage statistics (NFTs are coming in hot but we’ll save those for another day). So, given that, does 4.7% feel too low? Yes, probably. Could 4.7% double from here over the next year? Easily. Would that doubling occur while the total pie also doubles or more? Yes. Does that make DeFi unequivocally interesting, at least for a trade? Yes it does. Is there real regulatory risk on some of thus stuff? Yes there is.

Source: TradingView. As of 3/1/21.

This DeFi mania has also set the stage for a different trade that’s been playing out YTD. DeFi is causing ETH gas fees to skyrocket. On a single day, February 23rd, ETH users paid $50mm in fees. Mean fee of $38 and median of $19. Totally insane.

Source: Glassnode. As of 3/1/21.

That clogging of the ETH network and the commensurate spike in gas fees to egregious levels has driven large YTD outperformance for Layer 1 smart contracts platforms with high throughput capacity. The thesis of the trade is very simple. ETH is too slow to grow DeFi. These other blockchains are faster. Go rebuild DeFi on other Layer 1’s and take market share from ETH.

Source: TradingView. As of 3/1/21.

ETH. DeFi. Layer 1’s. NFTs. These are all classic bull market trades. None of this stuff works in 2018 when BTC isn’t working. This time around, the setup is even more well defined. The assumption is still that Bitcoin moves in four-year cycles centered around the halving. Maybe Bitcoin doesn’t do a blow off top and a massive retracement this time around, but if it doesn’t that will be the first time it’s ever acted like that. Now the market participants are different this time, so maybe it doesn’t blow off, we’ll see. Investors have a wide range of price targets but $100k is generally the low end and maybe $300k is the high end for this cycle. That’s a +100%-500% return from here. This setup is pretty different than prior cycles, because no one had a good handle on price targets for BTC or anything else back then. The base cases and upside cases were essentially undefined, or more accurately, blown through. And importantly, the expected returns for BTC vs ETH or LTC or QTUM or whatever else were not that well defined in 2017. Many investors look at the expected base case returns of BTC in the 100%-200% range and just think that’s not enough meat on the bone. If they wanted a double they’d go buy SPACs or weed stocks or SAAS calls. Ya know, something safer than Bitcoin…. So they begin to look elsewhere for things in crypto that have some real juice left in them – the elusive 10 bagger. My guess is this appetite has some legs left to it. If Bitcoin does a blow off top somewhere between 9/30/21 and 6/30/22, that’s PLENTY of time for DeFi dominance to go to 10% or even higher (assuming Gensler doesn’t get in and ruin the party, which is possible).

What happens after that will be the painful part. If BTC blows off and pulls back >50% as it has six times before, DeFi names will likely get demolished. Do you know what a down 75% move looks like? It looks like getting cut in half and then getting cut in half again. We will see plenty of those in DeFi if and when a cyclical top and correction comes for BTC. Act accordingly.

Closing Remarks

Call a spade a spade. February 2021 was one of the most impactful months in crypto history. There’s the saying “gradually, then suddenly.” This is the suddenly part. It’s easy to lose sight when you’re neck deep in it all day like we are, but make sure to appreciate the forest through the trees. This is what mass adoption of Bitcoin looks like. This is the scenario we dreamed about for years. It is the *required* backdrop for Bitcoin to achieve a trillion-dollar market cap and to go from $1tn to $2tn and beyond. It is that institutional Bitcoin adoption that is allowing for the innovation in Alts and DeFi to be so handsomely priced. And that’s fine. But make no mistake, this is Bitcoin’s world.

Bitcoin’s world is surrounded by the actual world. That’s a world where central banks and governments are going full gong show with their monetary and fiscal policies. A world where those in charge of making the money and spending the money have stopped asking the question “how are we going to pay for all of this?” It’s a world where those same central bankers and government officials have been backed into a corner by financial markets – they cannot tighten policies back up to even somewhat reasonable levels by historical standards, as it will cause a global collapse in asset prices and send the entire world into a deep depression. So they will keep going as they have been, and hopefully kick the can far enough along so that when it’s finally time to pay the piper, it’s not their problem. It’s our problem. My generation’s problem.

This multidecade approach to how the money is created and how the money is spent has led to deep-seeded distrust by the people those government officials are meant to represent. The majority of Americans look at what’s happened in the last 50 years and it sure does seem like a system that is rigged for the rich to get richer. That was never the American ideal. The Founding Fathers were vehemently against this crony capitalism and bought off politicians. Yet here we are.

Source: FRED. As of 12/28/20.

This distrust has metastasized into other areas of society and those have been front and center as of late. A distrust of Wall St. (e.g., GameStop). A distrust of big tech companies (e.g., de-platforming). All of this interrelated. And crypto is right in the middle of it. The eventual outcome is up to us.

“Rather than chase the cat, take away the plate”

– Japanese Proverb

Travis Kling

Founder & Chief Investment Officer

Ikigai Asset Management

P.S.

Included below is an incomplete list of memorable tweets from the last month. Twitter is not investment advice and my views could easily be wrong. That being said, like it or not, Twitter matters for crypto. I have no interest in being a talking head for a living and babbling about on Twitter is a long way away from being a good steward of investor capital. However, this is a community with open-source software in its DNA, and participants want to crowd-source the truth. We are shepherds of this technology. Answers to fundamental questions about this asset class are not currently clear, so having a public platform to share your views with the community is important. After all, you’re helping shape the future :)

1. Ikigai Asset Management is the trade name for a collection of advisory and consulting businesses operated by Travis Kling, Anthony Emtman, and their team.

The information contained or attached herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. This email is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, service of Ikigai as well as any Ikigai fund, whether an existing or contemplated fund, for which an offer can be made only by such fund’s Confidential Private Placement Memorandum and in compliance with applicable law. Past performance is not indicative nor a guarantee of future returns. Please consult your own independent advisors. All information is intended only for the named recipient(s) above and is covered by the Electronic Communications Privacy Act 18 U.S.C. Section 2510-2521. This email is confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received this message in error please immediately notify the sender by return email and delete this email message from your computer. Copyright 2021 Ikigai Asset Management, LLC. All Rights Reserved.

NOT INVESTMENT ADVICE; FOR INFORMATION ONLY

PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS